After the Blockade: 5 Counter-Intuitive Truths About the Reopening of the Strait of Hormuz

We have watched oil prices spike to a staggering $170 per barrel in March, witnessed the systematic depletion of strategic reserves,

For three months, the global economy has been held hostage by a silent chokehold on the world’s most vital energy artery. We have watched oil prices spike to a staggering $170 per barrel in March, witnessed the systematic depletion of strategic reserves, and felt the “misery” of energy-driven inflation from Manila to Manchester. Now, as a peace resolution finally flickers on the horizon, the markets are exhaling in anticipation of a “return to normal.”

However, investors expecting a binary reset are likely to be caught off guard. The reopening of the Strait is not a light switch; it is a complex, multi-layered unwinding of structural shifts and logistical scars. To navigate the post-blockade era, one must look past the immediate relief of the headlines and understand the new rules of the global energy map.

The Mirage of Immediate Flow: Why Peace Doesn’t Mean Supply

The assumption that a diplomatic signature immediately restores commodity flows is a dangerous oversimplification. Restoring normal conditions will be a multimonth—or even multiyear—process requiring tens of billions of dollars in remediation. Shipping lanes must be cleared of mines, targeted infrastructure requires reconstruction, and production facilities must be carefully stabilized.

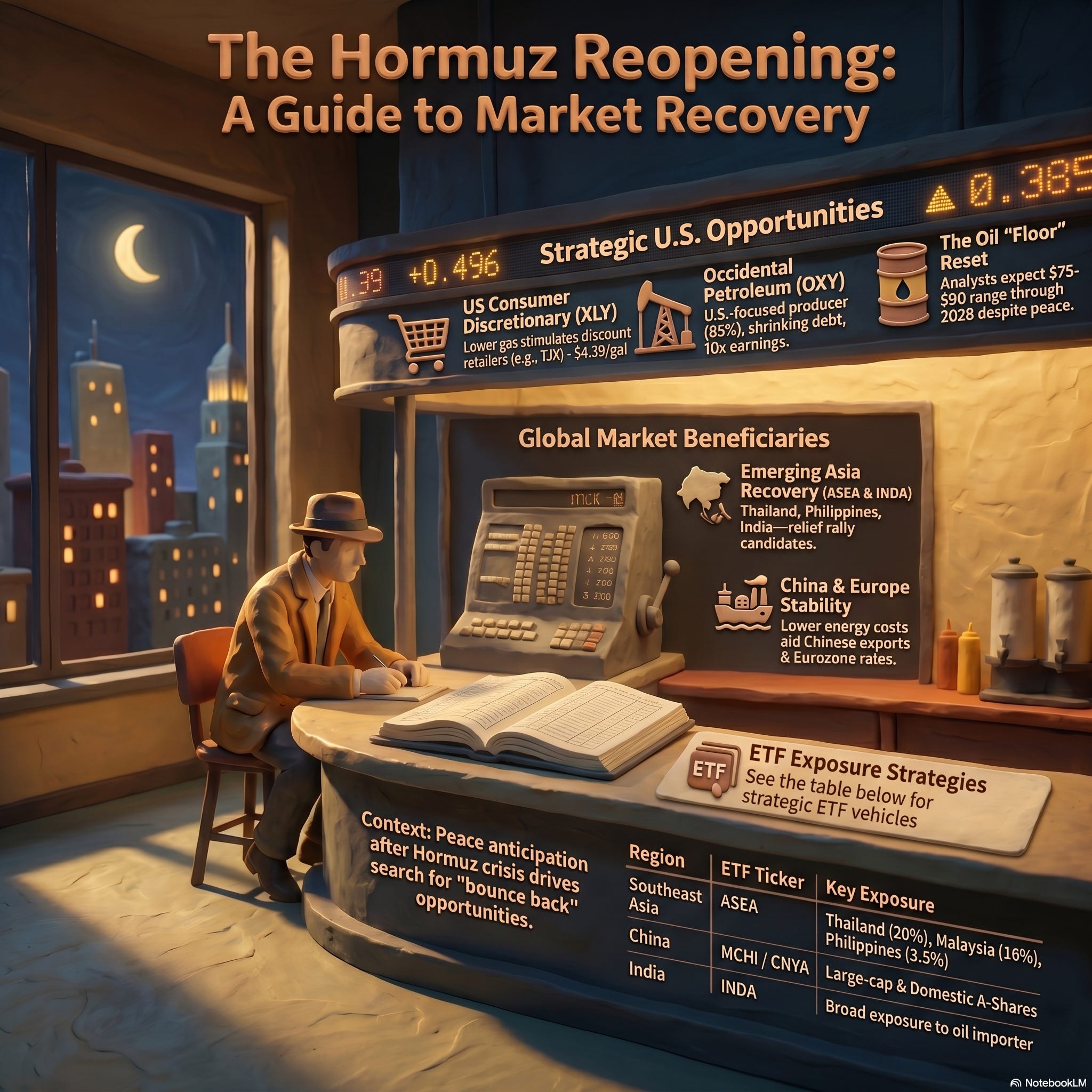

While the “geopolitical risk premium” that drove prices to $170 is already fading, a structural supply deficit remains firmly in place. Governments that aggressively tapped their Strategic Petroleum Reserves (SPR) to survive the blockade must now pivot from being sellers to being massive buyers to restock. This shift ensures that the eventual floor under oil prices will settle significantly higher than pre-conflict levels.

“Markets may be underestimating the time required to restore normal conditions,” warns Ole Hansen, head of commodity strategy at Saxo Bank. “A cease-fire may reopen shipping lanes, it does not immediately replenish inventories, restore damaged infrastructure or normalize trade flows.”

The Buffett-Backed Fixer-Upper: Why OXY Wins the Peace

In a “higher for longer” energy environment, the smartest play isn’t necessarily the most stable giant, but the most improved one. Occidental Petroleum (OXY) currently trades at roughly 10 times expected earnings, looking remarkably cheap compared to XOM (Exxon Mobil) or CVX (Chevron). While once criticized for its debt-heavy acquisition of Anadarko, OXY has whittled its debt down to $13.3 billion, rapidly closing in on its $10 billion target.

The “Buffett factor” remains a central pillar of this story, with an $8.8 billion obligation to Berkshire Hathaway (BRK.B) carrying a hefty 8% dividend. Analysts expect OXY to produce enough cash in the coming quarters to clear this hurdle, effectively transforming from a “problem child” into a debt-free cash machine by the end of the decade. With 83% of its production based in the U.S., it captures the upside of 80-90 crude while avoiding the operational risks still plaguing Middle Eastern producers.

The “Ghost” Fleet: Why Sanctions Failed the Storage Test

Throughout the crisis, the mainstream narrative suggested that the U.S. naval blockade had forced Iran into a production shutdown due to a total lack of storage. The data tells a more resilient story. Even after 46 days of the blockade, Iran maintains approximately 37 million barrels of available floating storage capacity, proving it has ample room to keep pumping despite the pressure.

Tehran’s ability to sustain itself is bolstered by a sophisticated “shadow fleet” and Hong Kong-based corporate networks that facilitate trade away from Western oversight. More than 30 Iran-linked tankers successfully broke through the blockade during the height of the tension, suggesting traditional sanctions are increasingly toothless. This hidden buffer means Iranian exports could flood back into the market more steadily than the “forced shutdown” theory ever predicted.

The Slingshot Effect: From “Miserable” to Mandatory

Currently, Chief Investment Officers describe the Southeast Asian landscape as “miserable,” but for a macro strategist, misery is often a synonym for opportunity. Countries like Thailand, where oil imports account for 7% of GDP, and the Philippines, currently battling “twin deficits” in both fiscal and current accounts, have been the primary victims of the blockade. This economic strain has suppressed valuations, setting the stage for a violent “recovery bounce” as energy costs retreat.

The Global X FTSE Southeast Asian ETF (ASEA) is the primary vehicle for this slingshot effect, offering heavy exposure to the regions most sensitive to an energy reprieve. Similarly, China’s MSCI China ETF (MCHI) and the A-shares focused CNYA offer a compelling play on the reduction of global slowdown risks. China has navigated the crisis better than most by diversifying into renewables and building a massive strategic cushion, but a Hormuz resolution removes the export-growth ceiling that has recently capped Chinese equities.

The $170 Lesson: Shale’s “Swing Producer” Status is Dead

The most startling realization of this crisis was the failure of U.S. shale to respond to record-high prices. When spot prices surged past $170 in March, U.S. production remained remarkably flat, ending the myth of shale as a flexible “swing producer.” This stagnation is rooted in high natural decline rates and a profound sense of “sovereign risk” among domestic drillers.

Producers are increasingly hesitant to commit capital when projects like South Bow‘s Prairie Connector face the same political uncertainty that doomed the Keystone XL. Furthermore, a critical “grade mismatch” exists: the world lost “medium sour” barrels from the Middle East, a grade primarily produced in the Gulf of Mexico, not the “light sweet” crude coming out of shale patches. Consequently, the U.S. cannot simply “drill its way out” of the next supply shock, leaving the global market perpetually vulnerable.

The Long Tail: A Permanent Era of Volatile Supply

The resolution of the Hormuz blockade will bring immediate relief to global indices like the SPX, but the strategic map has been permanently redrawn. We are seeing the long-term consequences of energy insecurity: Japan’s imports have hit their lowest levels since 1962, and nations everywhere are accelerating their move away from Middle Eastern dependency.

As we move past the immediate crisis, we must confront a sobering reality: the old rules of rapid price corrections and reliable swing production are relics of a bygone era. We are entering a permanent era of volatile supply where “returning to normal” is not a destination, but a long, expensive migration. The question for investors is no longer when the oil will flow, but who is best positioned to thrive in a world where energy remains a constant geopolitical weapon.